Putin believed that by invading Ukraine and engaging in wars in the East, he was restoring Russia's great power status. The result was Moscow's long-term loss of influence.

Putin's own-goal: after invading Ukraine, Russia lost its influence in Europe

As of January 1, 2025, Ukraine has blocked the transit of Russian gas on its territory. Factoring in other events in the wider Black Sea region and the Middle East, Kyiv’s decision could mark the end of Europe's energy dependency on Russia.

It is dependency whose early days can be traced back to the last decade of the 19th century, when the Tsarist Empire was developing into a major supplier of oil and coal to a fast-growing European industry. The 1973 oil embargo imposed by Arab countries in turn determined European nations to turn to Russian energy sources.

Russia’s attack on Ukraine in 2014 fundamentally complicated European-Russian relations, making it difficult for the former to continue a “business-as-usual” relationship with an aggressor and increasingly anti-democratic state. However, it took Russia’s large-scale invasion of 2022 for Europeans to truly understand that Russia cannot be persuaded to abide by international rules through dialogue alone, and must therefore be subjected to economic pressure, which implies, among other things, reducing purchases of Russian energy products, given that Moscow uses the money obtained from their sale to finance its war.

However, sanctioning Moscow’s aggression is but one side of the problem. Knowing that Europeans depend on their gas, the Russians have sought weaponize this dependency: if you don’t want us to cut off your gas, let us mind our own business. Moscow’s attempted blackmail further stressed the need for Europeans to eliminate their dependency on Russian energy imports. Recent developments in the Mediterranean and Middle East suggest that Europe’s shift towards non-Russian energy sources may be sustainable in the long term.

However, we are not just witnessing the end of this era of dependency. We may in fact be witnessing the gradual and definitive decline of imperial Russia as an idea and as a major source of influence in the wider, now interconnected region that includes Eastern Europe, the Black Sea, the Middle East and the Eastern Mediterranean. Putin’s losing strategy has turned Russia into an actor without reliable capital, an key element in international affairs. On the contrary, Russia has become a threat to almost all of its neighbors and beyond - let's not forget that Russia has been seeking for years to destabilize the West through attempts to influence elections and disinformation campaigns aimed at undermining liberal democracies, as well as international institutions and organizations. Russia is suspected of sabotage actions targeting submarine infrastructure and more. Russia has financed terrorist attacks and a series of assassination attempts against the US military and coalition members that intervened in Afghanistan.

Putin’s defeat in Syria helps Europe secure its energy demand

In 2015, Russia launched an ambitious military operation in Syria, a move designed not only to rebuild Moscow’s influence in the Middle East, but also to show that it has the capacity to be a global power. Russia’s involvement helped Bashar al-Assad turn the war to his favor. For several years, Russia’s strategy of allying itself with totalitarian regimes associated with terrorist groups seemed to pay off, as Iran, Syria, and their non-state allies (Iraqi Shiite militias, the Houthis, Hezbollah, Hamas and Islamic Jihad) came to control much of the region, and many of their opponents were defeated or pushed back. For some time now, however, Iran has been sustaining one defeat after another. In Syria, Moscow seems on the verge of losing its only foothold in the Mediterranean after the Bashar al-Assad regime collapsed, practically overnight – without the Russians lifting a finger to help. In my opinion, the blows Israel has dealt to Moscow’s two allies after October 7, 2023, have been instrumental, suggesting that Israel, jointly with the USA, will continue to dictate the regional agenda in the new era.

Russia’s loss of Rusia and the installation of a stable regime that the West can talk to might open (or, rather, reopen) important possibilities for accessing resources in the Arabian Peninsula and the Persian Gulf area, but also in the Eastern Mediterranean. This would ensure long-term energy security for Europeans and would make Russian gas irrelevant to the EU.

For the time being, we are witnessing a rebalancing of power relations in the Middle East. Certain actors are becoming more influential compared to recent years (the USA, Israel, Qatar, Saudi Arabia, Egypt, the United Arab Emirates, and perhaps Turkey as well), while others are gradually losing their relevance, without fully disappearing from the picture. Russia and Iran are backed into a corner, but they can still threaten the stability of the Middle East. For instance, with Tehran's support, the Houthi rebels continue to affect the security of maritime traffic through the Bab-el-Mandeb Strait to the Red Sea and the Suez Canal. About 30% of the world's container trade passes through this area, not to mention other important trade flows, such as oil and other raw materials. In turn, Sunni Muslim extremists, especially those associated with Al-Qaeda or the Islamic State, continue to pose a threat to the entire Middle East. Thousands are held in prisons controlled by the Syrian Democratic Forces (SDF), dominated by the Kurdish PYD militia, but the PYD is under immense pressure from Turkey over its links to the PKK. According to Ankara, any arrangement for a final peace in Syria must exclude the PYD, even though this Kurdish faction was and remains the USA’s main ally against Sunni extremists, controlling the northeast, where it protects millions of Kurds.

The gas reserves in the Eastern Mediterranean, the EU, Turkey and the Cyprus question

Adding to this already complicated picture is the significant energy potential of the Eastern Mediterranean, where offshore natural gas deposits have been discovered. The gas will be enough to supply the countries of the region and Europe for many years. However, the exclusive economic zones in the Mediterranean need to be clarified, and only now can this issue be addressed with Damascus and Beirut at the table, without them actually representing the interests of Moscow and Tehran.

After the interruption of pipeline-delivered gas supplies from Russia, Europe needs alternative energy sources for its transition to a fully green economy, and the Eastern Mediterranean represents such an alternative. Turkey, in particular, has its own plans. Ankara's so-called neo-Ottoman agenda, disguised as the “Blue Homeland” (Mavi Vatan) doctrine, remains a threat to any project designed to bring stability to the region. The logic of this doctrine includes all aggressive actions against Greece and Cyprus, from naval exercises and perpetual shenanigans in the Aegean Sea, to exploring new hydrocarbon pockets in exclusive economic zones disputed with Nicosia and Athens. Turkey's 2019 agreement with Libya to delineate the exclusive economic zone in the Eastern Mediterranean not only violates the principles of the United Nations Convention on the Law of the Sea (UNCLOS), but is almost explicitly designed against the interests of Greece, Cyprus and Egypt. At present, some have voiced well-founded fears that a similar agreement could be concluded with the new regime in Damascus, which owes Ankara much of its current success.

The consequences might be particularly dire with regard to the natural gas reserves in the eastern Mediterranean, which are of interest not only to the states in the region, but also to the European Union. Currently estimated at several trillion cubic meters, with over 2 trillion in Egypt’s maritime zone alone, and almost 1,000 in that controlled by Israel, these reserves could represent a definitive alternative to Russian gas supplies for Europe. Given that the construction and operation of gas pipelines are increasingly perceived as economically inefficient solutions, the industry is starting to favor two possible alternatives: (1) exports of liquefied gas (LNG); (2) the production of electricity in gas-fired power plants and the export of the energy produced via high-capacity cables. In the case of the Eastern Mediterranean, both solutions are viable. Another high stake is also the final inclusion of Cyprus in the European energy network, by connecting it to Greece. However, Turkey is taking advantage of the political difficulties on the island and in the region.

In short, Ankara no longer supports the solution agreed under the auspices of the UN, of a single unitary state for the two nations, but rather that of two independent states, with separate jurisdictions and sovereign rights, both on land and at sea. In addition to the problems created by the Turkish-Libyan agreement on the delineation of exclusive economic zones and a possible similar Turkish-Syrian agreement, this could complicate the situation in the long term. Not all states in the region will be able to conclude agreements on tracing exclusive economic zones, thus postponing the projects for the exploitation of gas fields in the Eastern Mediterranean.

Alternatives for Europe: increasing LNG and electricity imports

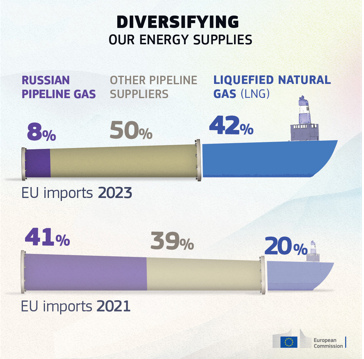

Meanwhile, an increasingly important alternative is the global supply of LNG, and European demand for this product has increased, to the detriment of pipeline-delivered gas. A major exporter like Qatar, for example, recently made it very clear that it has abandoned the idea of transferring gas to Europe through pipelines that pass through unstable countries, such as Syria or Iraq, and then through Turkey. Meanwhile, the European Union and some of its member states have already invested heavily in the construction of liquefaction/gasification facilities which would allow it to receive increasing volumes of LNG. The latest such terminal, built on the island of Krk in Croatia, adds to an increasingly wide network. And the share of LNG in Europe’s natural gas imports has increased to over 40%, from 20% in 2021. The largest exporter is now the USA, but there are also other important suppliers, such as Gulf countries or some countries in Africa (Nigeria, Egypt or Algeria), in addition to Australia, Indonesia, Malaysia or Trinidad and Tobago.

Other alternative sources for Romania and Europe are already taking shape in the Black Sea area, and are also close to the criteria for green energy. In just a few years, we will have access to electricity produced based on natural gas imported from Azerbaijan and then transferred to the West via a submarine cable transiting the Black Sea. On the other hand, considering all of the abovementioned elements, there are no major investments in store, meant to expand the transfer capacities of existing pipelines, such as TANAP (from Azerbaijan), Blue Stream and Turk Stream 1 and 2 (from Russia). Each of these pipelines will continue to transfer between 15 and 30 billion cubic meters of gas to Turkey annually, with only half of this amount then going to Europe. At any rate, this is hardly enough. Although the EU’s annual gas input has been steadily decreasing with the share of renewable resources increasing in recent years, it still rose to around 300 billion cubic meters in 2023.

A missed learning opportunity: although Russia has just one pipeline left for exports to Europe, it’s still trying to play it strong

Turkstream 2 remains the only pipeline officially delivering Russian gas to Europe, after gas transit through Ukraine was discontinued. This pipeline, which crosses the Black Sea, is already operating at full capacity (15 billion cubic meters per year). It transfers a so-called “Turkish Blend” in which Russian gas has a significant share, mixed with deliveries from the Caspian region. But its maximum capacity barely covers the needs of 2-3 states in the Balkan region.

In addition, Moscow can no longer with be negotiated with, continuing to be hostile even towards its allies. On December 28, 2024, Gazprom announced it was unilaterally interrupting gas supplies to the Republic of Moldova, citing unpaid debt. This so-called debt was actually created by Moscow, which for years supplied natural gas to Transnistria for free, but claimed that the authorities in Chișinău must foot the bill. The government in Chișinău estimated its own debt to Gazprom at only 3 million USD, not 700 million, as the Russian energy giant claims.

The entire affair seems to be an attempt from Russia to destabilize the Republic of Moldova, which can endure only by connecting to European energy networks and, politically, by continuing its European accession efforts. However, the Kremlin's pressures are expected to intensify, both in terms of energy and politics, with the approaching parliamentary election in the Republic of Moldova this summer. The situation in the neighboring country shows that the Putin regime remains an extremely dangerous actor for European democracies, even after Europe reduced its dependency on Russian natural gas. Russia may have lost some of its influence, but it is still capable of blackmail through other means.

The situation remains extremely volatile and the details presented here do not serve as conclusions. What is clear, however, is that Kyiv’s bold decision not to prolong the contract with Gazprom further isolates Russia, reducing its overall regional influence. But Putin has made a lot of miscalculations over the past two decades, probably failing to grasp the long-term strategic consequences already taken by Brussels. Despite all the mistakes made by the European Union, its policies have generally stimulated the diversification of energy resources and the gradual transition to an increasingly green economy. Overall, the share of gas transiting Ukraine had already fallen from 11% in 2021 to just 5%. All the while, Ukraine’s decision to end gas transit on January 1, 2025 deprives Russia of revenues worth approximately 6.5 billion USD.

The only European states that still depended on Russian gas were Slovakia, Austria and Hungary. Of these, Slovakia and Austria have developed alternative sources in the past two years. Hungary will continue to cover part of its gas demand with imports from Russia via Turkstream 2. However, all three countries, together with the other EU member states, benefit from being connected to the European energy network and market, where distribution and prices are regulated by supply and demand, not by the blackmail of the authoritarian neighbor to the east. Europe continues to diversify its resources, and when it comes to imports from outside Europe, LNG and electricity will most likely continue to grow, to the detriment of classic pipeline imports. Nevertheless, access to reserves that are geographically closer to Europe, such as those in the Eastern Mediterranean, now depends on regional political developments. Based on all the details presented above, it would be possible for an actor such as Turkey to increasingly use its strategic position to press for advantages. However, it is also possible that the perception of such aggressive behavior would rather bring disadvantages to Ankara in its relationship with the European Union and some of its member states.

However, the Russian footprint is increasingly shrinking in the European energy sector and in the developments in the wider region. Beyond Moscow’s widespread manipulation of nationalist-extremist groups in Europe, which now seem to be successful, we may actually be witnessing the start of the definitive decline of Russian imperialism in this part of the world.

{kind=link}